Business performance headed south

Although the energy crisis loosened its grip on European economies, rampant inflation and general uncertainty continue to weigh heavily on the European plastics industry along the whole value chain. Almost half of the survey participants said their companies did worse in H1 2023 compared to H2 2022, with only 28.7% reporting some improvements; 25% noted no tangible changes. Things have been going downhill for a while now – in the second half of 2022, nearly half of the respondents admitted worsening business performance, while only 26.7% said things were looking up.

Not all regions are in the same boat, as no surveyed companies in France, Spain, Portugal, the UK, and Ireland reported their operations deteriorating. The majority of companies in the Benelux, Central and Eastern Europe, and Italy reported weaker business.

In terms of sectors, the situation seems to have been particularly dire for recyclers, which is no surprise given falling prices for virgin plastics and huge cost pressures. Over 70% cited less business in H1 compared to H2 2022, with none reporting an improvement.

Upswing might be around the corner

Despite H1 2023 falling short of expectations, the industry seems to be expressing cautious optimism. In H2 2023, over 29% of the surveyed companies predicted an upward trend compared to H1 2023. As in the first half of the year, a majority said they anticipate no substantial shifts in either direction, while 21.6% shared a pessimistic outlook. In general, the mood in the industry has mostly stayed the same since H2 2022.

The forecast for exports remains the most conservative, pertaining to sales within Europe, where 57.7% of companies expect no changes.

The strongest optimism was observed in Spain, Portugal, and the Benelux. In addition, no survey participant from German-speaking Europe, Italy, and Central and Eastern Europe said they anticipated new blows on the horizon. And yet again, plastics recyclers failed to forecast improvements over the next months. Resin producers and converters are also unable to see things improve anytime soon, while more plastics products traders (33%) projected better performance than the industry average, even though half of the latter group was still pessimistic.

Investment strategies remain conservative

The economic reality also pushed market players to be prudent about spending money. While almost half of the survey participants said their companies’ short and medium-term investment plans remained unchanged in H1 2023, over 31% admitted to cutting their budgets.

Only 19.7% of those surveyed claimed they spent more than in H2 2022.

Across the region, investment activity was higher in Southern Europe and lower in the Benelux and Nordic regions. In the sectoral split, companies working in plastics recycling and recovery appeared most willing to invest, while businesses engaged in plastics products trade, raw materials distribution, and compounding took the most cautious stance.

Staff remains unchanged

As European economies keep struggling against persisting labour shortages, staffing across the plastics industry was little changed.

A majority of respondents stated that the number of employees in their companies held steady in H1. Slightly more companies dismissed workers than hired new ones: 26.2% for the former and 19.3% for the latter.

On the Iberian peninsula, 40% of those surveyed expanded staff, and no respondents reported layoffs. In contrast, no increases were seen in Southeast Europe, Italy, German-speaking Europe, and the CEE. Among the companies with more than 500 employees, 15.5% hired more than they let go, while for almost 38% of businesses, it was the other way around. At the same time, companies with a staff of up to 20 workers seem to forge stronger ties within the working teams, as 87.5% of respondents in this segment reported no changes in the number of employees.

Looming uncertainty over inflation rates and the state of play in the global market seemed to push more operations to delay staff changes.

In the second half of 2023, the share of companies along the plastics value chain planning to keep employee ranks at the same level totaled 65.7%, which was close to expectations seen at the end of 2022 for the first six months of 2023.

In comparison with the previous survey, the picture turned slightly gloomy, as the share of companies expecting layoffs jumped from 13.2% to 19.3%, while those planning new hirings dropped from nearly a quarter to 15%.

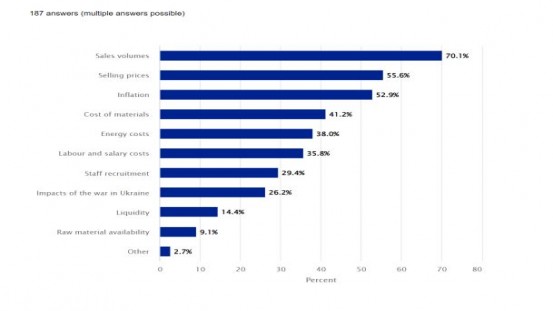

Weak market, inflation distress businesses

While in H2 2022, managers primarily expressed concerns associated with the meteoric rise in energy costs, sales market turbulence is steadily coming to the fore in 2023.

As many as 70% of survey participants seem to be primarily worried about the (low) sales volumes, with about 55% believing they will be troubled by selling prices, and almost 53% being worried about inflation in H2 2023. Cost-related concerns are about to fade into the background, as only 41.2% of those surveyed think they would be bothered by the cost of materials and slightly more than a third by energy costs, labour, and salary costs.

In H1 2023, sales volumes seemed to be an issue for 63.3%, inflation for 59%, and selling prices for over 51% of the surveyed companies. The cost of energy and raw materials bothered nearly every second respondent, while labour and salary costs were a concern for every third.

Ongoing crisis changes sourcing strategy

As international forces whipsaw prices with increasing frequency, plastics processors are having to adjust their ordering practices accordingly.

Less than 31% of respondents said their purchasing strategy had not changed, and more than 8% said they didn’t generally purchase resin, which means over 60% of those polled took a different tack when it came to buying product. The survey results show that 9% of companies exclusively use the spot market, more than 28% are shifting to that market by signing fewer contracts, and over 17% said they are dropping deals that are longer than a year in favour of those with a shorter timeframe.

Around 46% of those polled said the shift toward spot purchasing has also affected their sourcing, with 23% noting that they have expanded their supplier pool, over 18% saying they have bundled procurement to achieve economies of scale, and more than 5% reporting a change in suppliers.

Hope continues for return to pre-crisis levels in 2024

The words of former US disc jockey Casey Kasem are perfect for describing the seemingly countless events that have been battering the global economy, starting with the pandemic: the hits just keep on coming.

Wars, inflation, recessions, rising borrowing costs, chaotic weather, and a host of other factors have left many managers unsure about their company’s prospects. According to the latest PIE poll, only 9.5% of respondents said they have recovered to pre-crisis levels, and nearly 4% said they were not affected. That leaves around 86% that have yet to fully rebound, with over half saying they do not expect to match their pre-pandemic activity until next year. Less than 6% predict a return to previous levels in the second half, almost 7% forecast that they will never reach that mark again, and more than 17% cannot even venture a guess.

About the PIE Market Survey:

To gauge how business is developing in the European plastics industry, PIE conducted its 10th Market Survey. The questionnaire was made open to PIE subscribers and other industry players and saw almost 200 participants from across Europe.